Renting your property for a film shoot involves unique risks that standard insurance won’t cover. From property damage to legal disputes, having the right insurance is critical. Here’s what you need to know:

- Why Insurance Matters: Film shoots involve crews, heavy equipment, and potential liabilities. Without proper coverage, property owners face financial risks.

- Key Policies:

- Commercial General Liability (CGL): Covers third-party injuries and damages. Minimum $1M per occurrence, often higher for luxury properties.

- Property Damage Insurance: Protects against damages to the filming location, especially crucial for high-end properties.

- Equipment & Vehicle Insurance: Covers theft or damage to production tools and vehicles.

- Workers’ Compensation: Required for crew injuries.

- Drone Insurance: Needed for aerial filming.

- Luxury Property Risks: High-value assets like marble countertops or sculptures require additional protection, including "loss of use" coverage for lost rental income during repairs.

- Contracts: Ensure a location agreement includes indemnification clauses, primary insurance language, and waiver of subrogation.

- Documentation: Request Certificates of Insurance (COIs) and endorsements to verify coverage, and document property conditions before and after filming.

Proper insurance, thorough documentation, and clear contracts can protect your property and income during film shoots.

The basics of production insurance for film with Stacie O’Beirne

sbb-itb-161ccc1

Key Insurance Policies for Film Productions

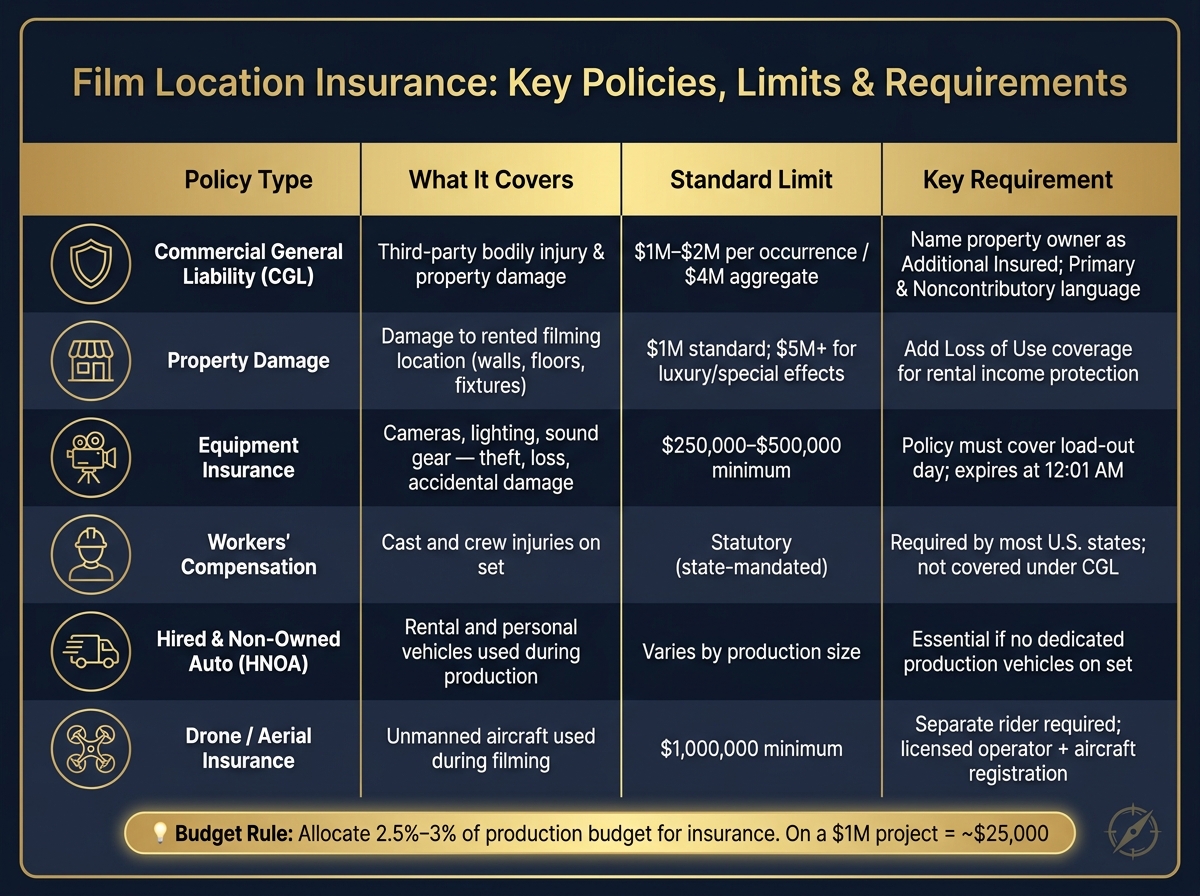

Film Location Insurance: Key Policies, Limits & Requirements

Understanding the right insurance policies can save film productions from unexpected financial setbacks. Film shoots come with a variety of risks, and no single policy can cover every scenario. Below, we’ll break down the essential insurance policies that make up a solid coverage plan for film productions.

Commercial General Liability (CGL) Coverage

CGL is the cornerstone of insurance for film productions. It protects against third-party bodily injuries and property damage. For example, if a crew member accidentally damages a neighbor’s car or a bystander trips over a cable on set, CGL can help cover legal and medical costs.

Most CGL policies provide coverage starting at $1 million per occurrence, with higher-end productions often requiring $2 million or more. For shoots in public locations, an umbrella policy of up to $5 million might be necessary to address heightened risks.

Property owners often require productions to meet two key terms: naming them as an Additional Insured and including primary and noncontributory language to ensure the production’s policy pays first.

"The Producer shall maintain at its sole cost and expense Commercial General Liability insurance with limits not less than $2,000,000 per occurrence and $4,000,000 aggregate, naming the Owner as an Additional Insured." – Viral.Villas

It’s important to note that CGL does not cover injuries to the cast or crew. These are typically handled under Workers’ Compensation, which is mandated in most states.

Property Damage Coverage for Film Locations

While CGL handles third-party claims, property damage coverage protects the rented filming location itself. This includes damage to walls, floors, fixtures, and other unique architectural elements. This type of coverage is especially critical for high-end properties, where even minor incidents can lead to costly repairs.

Most property damage policies start at $1 million, but luxury estates or productions involving special effects like pyrotechnics or rain towers may require limits exceeding $5 million. Separate riders are often necessary to address these specific risks.

"If a rented property or filming location is damaged during production, [General Liability] will cover the cost of repairs." – SetHero

For property owners, adding loss of use coverage – which compensates for rental income lost during repair periods – can provide significant financial protection, particularly for high-value properties.

Equipment and Vehicle Insurance for Productions

Equipment insurance safeguards essential production tools – cameras, lighting, sound equipment, and more – against theft, loss, or accidental damage. Coverage typically applies from the time equipment leaves the rental house until it’s returned. Deductibles range from $500 to $5,000, and many rental companies require productions to carry at least $250,000 to $500,000 in equipment coverage.

It’s also worth noting that most equipment policies expire at 12:01 AM on the expiration date. For instance, if equipment is due back on a Friday, extending the policy through Saturday ensures no gaps in coverage.

Vehicle insurance is another critical piece. Standard auto policies often don’t cover incidents involving rental or personal vehicles used on set. Productions should confirm Hired and Non-Owned Auto (HNOA) coverage to protect these vehicles. Additionally, if drones are used for aerial shots, a separate drone insurance rider is required, as standard equipment policies don’t cover unmanned aircraft.

| Policy Type | What It Covers | Key Consideration |

|---|---|---|

| Commercial General Liability (CGL) | Third-party injury and property damage | Require Additional Insured status |

| Property Damage | Damage to the rented location | Increase limits for luxury features |

| Equipment Insurance | Cameras, lighting, and sound gear | Check policy expiration timing |

| Workers’ Compensation | Injuries to cast and crew | Required by most U.S. states |

| Hired & Non-Owned Auto | Rental/personal vehicles used on set | Essential if no dedicated production vehicles |

| Drone/Aerial | Unmanned aircraft used during filming | Separate rider required |

These policies form a solid foundation for managing risks and ensuring smooth operations during film productions.

Identifying and Reducing Location-Specific Risks

How to Conduct a Risk Assessment

Plan a walkthrough with the production manager 14–60 days before the shoot to evaluate load-in routes, staging areas, and electrical capacity. This early inspection helps uncover potential problems, like flooring that can’t handle heavy equipment or shared corridors that might cause delays.

During this walkthrough, take note of the specific activities planned for the shoot. For instance, a small two-person branded shoot has far fewer risks compared to a larger 15-person commercial production involving drones, smoke machines, or generators. Bigger productions demand extra attention to factors like equipment parking, HOA restrictions, noise levels, and local permit requirements.

"The bigger the footprint, the more likely you need higher liability limits, written permission for commercial use, and explicit rules for staging, lighting, and guest access." – Maya Linwood, Senior Travel Editor & Creator Production Strategist

By identifying these risks upfront, you can create clear documentation and address potential issues quickly.

Common Loss Scenarios and Documentation

Film sets often encounter a handful of recurring issues: property damage (like equipment hitting custom millwork), third-party injuries, equipment theft, and vehicle mishaps involving grip trucks or production vans. Proper documentation is critical for managing these situations and supporting insurance claims.

Use timestamped photos and a mutual sign-off report to document the property’s condition before filming begins. This helps prevent disputes over normal wear and tear. After the shoot, conduct a follow-up walkthrough within 24 to 72 hours to confirm the property has been restored. Keep all permits, Certificates of Insurance (COIs), and incident reports for at least seven years to handle delayed claims or audits.

When budgeting, allocate about 2.5% of the production cost for insurance, typically with a $2,500 deductible. For context, feature film insurance can range from $2,000 to $15,000, while music video insurance might cost between $800 and $5,000.

Having a clear understanding of these scenarios helps property owners meet the higher insurance requirements often associated with luxury properties.

Meeting Insurance Standards for Luxury Properties

High-end properties come with greater risks, which means higher insurance standards. Standard Commercial General Liability (CGL) limits of $1,000,000 per occurrence and $2,000,000 aggregate often fall short. For luxury locations, limits of $2,000,000 per occurrence and $4,000,000 aggregate are more typical.

Additionally, certain endorsements are essential. A Waiver of Subrogation ensures the insurer won’t pursue the property owner after paying a claim – this is a common requirement for premium rentals. Productions involving drones should require licensed operators, aircraft registration, and drone-specific insurance with limits of at least $1,000,000. Be wary of productions that refuse to name the property owner as an Additional Insured, provide an expired COI, or plan high-risk activities like open-flame work without special-event coverage. These are clear red flags that could lead to significant liability issues.

| Risk Factor | Minimum Requirement | Elevated Standard (Luxury) |

|---|---|---|

| CGL per occurrence | $1,000,000 | $2,000,000 |

| CGL aggregate | $2,000,000 | $4,000,000 |

| Drone liability | $1,000,000 | $1,000,000+ |

Contracts and Documentation for Insurance Protection

To effectively protect your property during film productions, clear contractual terms and meticulous documentation are essential alongside proper insurance coverage.

Key Clauses in Location Agreements

A well-drafted location agreement is crucial – it establishes liability responsibilities and ensures all parties understand their obligations. One of the most critical elements is the indemnification clause, which requires the producer to take full responsibility for any claims, fines, lawsuits, or injuries that arise from the production’s use of the property. Without this clause, property owners could find themselves liable for incidents they had no control over.

Another must-have clause is one that designates the producer’s insurance policy as primary and noncontributory. This ensures their policy responds first to any claims, leaving the property owner’s coverage untouched. Additionally, include a waiver of subrogation to prevent the producer’s insurer from pursuing recovery against the property owner.

If outside vendors – like catering teams, lighting crews, or drone operators – are involved, the agreement should require them to carry adequate insurance as well. To maintain continuous protection, mandate 30 days’ written notice before any cancellation or non-renewal of policies.

These clauses lay the groundwork for the documentation requirements detailed below.

Certificates of Insurance (COIs) and Endorsements

Having proper insurance policies is only part of the equation. The contract language must reflect these standards, and documentation must confirm compliance. A Certificate of Insurance (COI) provides a one-page summary of the production’s active policies, listing the carrier, coverage types, limits, and dates. However, it’s crucial to note:

"The COI itself is not a contract; it summarizes the underlying policy. Hotels should request endorsement copies (CG 20 10, CG 20 37) for higher-risk activities to verify the additional-insured language is actually in the policy." – Latent Insurance

For productions involving higher-risk activities – like stunts, drones, or pyrotechnics – request endorsement copies (e.g., CG 20 10, CG 20 37). These documents formally amend the policy and confirm additional insured status. Also, ensure the COI’s "Description of Operations" explicitly states that the property owner and their agents are covered for filming activities. Double-check that the insured name on the COI matches the name on the film permit and rental agreement to avoid claim denials.

All COIs and endorsements should be provided at least five business days before production begins.

Here’s a breakdown of key documents and their roles:

| Document | Function | Legal Weight |

|---|---|---|

| Certificate of Insurance (COI) | Summarizes policy types, limits, and dates | Informational only; does not grant contractual rights |

| Endorsement | Formally amends the insurance policy | Authoritative evidence of coverage changes |

| Location Agreement | Contract detailing scope, fees, and liability | Primary risk-control document between the parties |

Aligning Insurance Coverage with Production Schedules

Coverage gaps often occur during critical times, like load-in or load-out, when crew and equipment are on-site but the insurance policy has not yet started or has already expired. To avoid this, ensure insurance coverage spans from the moment the first piece of equipment arrives until the last item is removed and the property is restored.

"All insurance policies expire at 12:01 am. So, for example, if you’re dropping off your equipment on June 1st, then the expiration date of your insurance policy should appear as June 2nd at 12:01 am, rather than June 1st." – Katherine Wong, Founder, Athos Insurance

Set policies to extend beyond load-in and load-out times. If production wraps on a Friday, consider setting the expiration to Saturday to cover any unforeseen delays. Adding one or two buffer days can account for weather issues, extended restoration work, or late equipment returns. To avoid last-minute surprises, verify COI dates with the insurer at least 14 days before filming starts.

How Luxury Platforms Help Manage Film Location Risk

Managed luxury platforms take the complexities of film location risk management to the next level. By going beyond basic rental agreements, these platforms, like Essentialyfe, provide a structured approach to address operational, logistical, and insurance challenges. This allows property owners and production teams to focus on the creative process while ensuring the location is protected.

Pre-Vetting Properties for Film Readiness

Accurate documentation is crucial, but luxury platforms refine this through a thorough pre-vetting process. Before a booking is confirmed, the platform evaluates both the property and the production team. This includes verifying the production company’s credentials, project details, and sponsors. Site walks with production managers are conducted to review critical elements like load-in pathways, staging areas, and electrical capacity. These checks help identify potential risks, such as overloaded circuits or areas prone to damage.

Additionally, contract templates undergo careful review to include key protections like restoration requirements, defined usage terms, and occupancy limits. The platform ensures that the production’s Certificate of Insurance (COI) names the property owner as an additional insured with appropriate language. Below is an outline of the vetting process:

| Vetting Step | Objective | When |

|---|---|---|

| Identity Verification | Confirm production company and project scope | 60+ days out |

| Site Walk | Approve load-in routes and power capacity | 14 days out |

| COI Audit | Verify "Additional Insured" status and limits | 14 days out |

| Pre-flight Photo Log | Document property condition for claims protection | 1–3 days out |

| Final Walk-through | Confirm restoration and release deposit | 48–72 hours post-wrap |

Risk-Reducing Services on Location

Once filming starts, on-site services provided by the platform help maintain safety and prevent incidents. A designated point of contact (POC) ensures smooth communication between the property owner and the production team. This POC also oversees vendor access, enforces safety protocols, and ensures compliance with rules like maintaining clear fire exits, proper cable management, and smoking restrictions. By centralizing these responsibilities, the risk of property damage or insurance coverage gaps is significantly reduced.

Luxury platforms also maintain pre-approved lists of insured and vetted vendors, including security personnel, licensed electricians, and certified drone operators. This ensures that production teams work only with professionals who meet industry standards. As one industry expert notes:

"Professional productions bring opportunity and predictability – but they also bring higher standards that you must meet to play at that level." – Viral.Villas

Essentialyfe further enhances this model with integrated security and shuttle services. Their trained staff, familiar with the property’s layout, help streamline access and maintain order during shoots.

Protecting Property Value Through Managed Film Shoots

Preserving the property’s value is a top priority, and a well-managed shoot ensures that the location remains in excellent condition. Pre-shoot and post-shoot walkthroughs, accompanied by timestamped photo logs, create a clear record of the property’s state. This documentation simplifies the resolution of any disputes related to deposits or damages.

Restoration clauses in agreements managed by the platform require the property to be returned to its original condition within 24 to 72 hours after filming wraps. This quick turnaround minimizes downtime and ensures the property is ready for its next booking, safeguarding its long-term rental income potential.

Conclusion: Steps to a Safe and Well-Insured Film Shoot

Safeguarding a luxury property during a film shoot boils down to three key elements: proper insurance, thorough documentation, and a well-defined contract. A good rule of thumb is to allocate 2.5%–3% of the production budget for insurance. For example, on a $1M project, that means setting aside around $25,000. While it may seem like a significant expense, it’s a small price to pay compared to the potential financial hit of an uninsured incident.

Double-check all Certificates of Insurance (COI) to ensure they meet the necessary criteria, including naming specifics, coverage dates, and "Primary and Noncontributory" status. Coverage should extend from the initial load-in to the final wrap. Additionally, keep all COIs, permits, and incident reports on file for at least seven years.

"Production insurance shields the production and, more specifically, the producer from any unexpected costs, such as equipment damage or lawsuits." – SetHero

Using a managed platform like Essentialyfe can simplify this process. These platforms handle everything from auditing contract templates and organizing site inspections to maintaining a list of vetted vendors and managing post-shoot walkthroughs. Their structured approach minimizes the risk of coverage gaps or disputes over damages.

FAQs

What insurance should I require from a production before letting them film at my home?

To protect yourself and your property during filming, require the production team to carry liability insurance. This covers potential injuries or property damage that might occur. Additionally, ensure they have property or equipment insurance to guard against damage or theft involving your home. These policies provide an extra layer of security and help reduce financial risks.

What’s the difference between a COI and an endorsement, and which one do I need?

A Certificate of Insurance (COI) serves as proof that an insurance policy is in place, but it doesn’t outline the specifics of the coverage. On the other hand, an endorsement changes the policy to clarify exactly who or what is covered. When renting a film location, an endorsement is usually required to address the unique risks and ensure the proper parties are included in the coverage. Relying solely on a COI won’t provide this level of protection.

How can I avoid insurance coverage gaps during load-in and load-out?

When planning your insurance coverage, make sure it protects your equipment and property from the moment it leaves the rental house until it’s safely returned. To avoid any gaps, your policy should begin on or before the load-in day and remain active through load-out. Ask for a Certificate of Insurance that clearly specifies these dates, and double-check with your insurer to confirm that every stage – setup, event, and takedown – is included for uninterrupted coverage.